Fuel Markets in Crisis: Germany’s Competition Law Response

March 25, 2026

In response to the sharp increase in fuel prices following the military conflicts in the Middle East, Germany plans a new bill with notable implications for competition law.

The new Fuel Policy Package (Kraftstoffmaßnahmenpaket) will likely be voted on in the German Parliament Bundestag tomorrow (26 March 2026) and comprises three core measures:

1) It introduces arts of the so-called (former) Austrian model, under which fuel prices at public petrol stations may be increased only once per day at 12:00 noon, while price reductions are permitted at any time.

2) It introduces a new form of exploitative abuse in the wholesale and refining fuel market, also covering cases of relative market power based on excessive mark-ups, alongside a reversal of the burden of proof in favour of competition authorities with regard to cost levels and their reasonableness.

3) It facilitates proceedings under Germany’s new competition tool (sector inquiries with remedies, see here, here, and here for the previous model introduced with the 11th Amendment Act) in two ways:

a) The former three-stage procedure – (1) sector inquiry, (2) a finding of a significant and continuing malfunctioning of competition, and (3) the imposition of remedial measures – is reduced to two stages, with the finding and the imposition of remedies combined into a single step.

b) In addition, the requirement that addressees of remedial measures must have ‘contributed significantly to the malfunctioning of competition’ through their conduct and their relevance to the market structure is removed; it will suffice that the Federal Cartel Office (Bundeskartellamt) may impose ‘any behavioural or structural remedies necessary to eliminate or reduce the malfunctioning of competition’.

Background

Ongoing military conflicts in the Middle East, coupled with disruptions to shipping traffic in the Strait of Hormuz, have led to a significant increase in global prices for crude oil and petroleum products. Many states are therefore considering regulatory intervention.

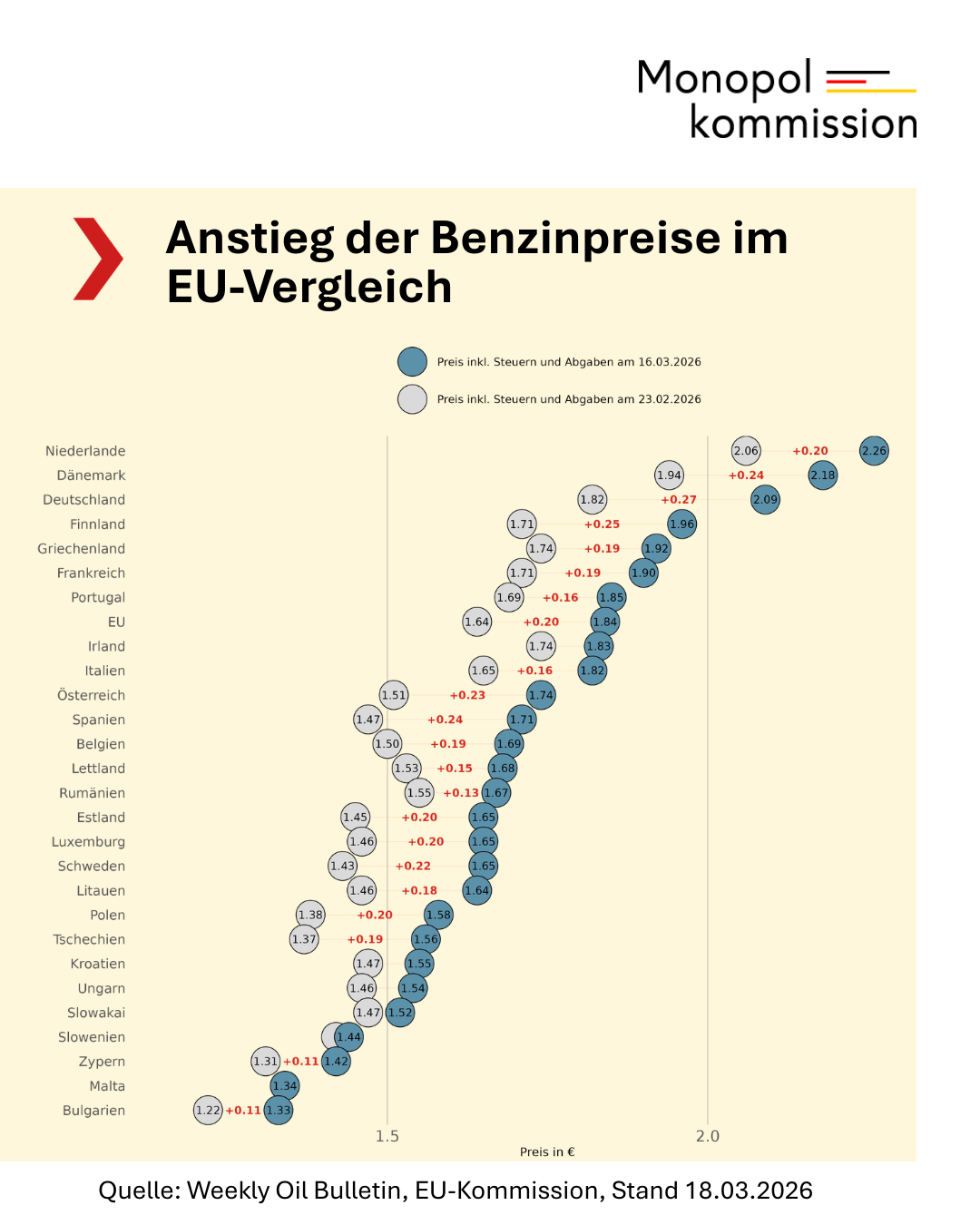

Image

(Source: Monopolies Commission)

Data from the German Monopolies Commission indicates that Germany appears to be affected more severely and more rapidly by fuel price increases than other EU countries. Consumers in Germany seem to be particularly impacted, as fuel prices at petrol stations have, in some cases, risen much more sharply than crude oil prices. The Monopolies Commission expressly notes that increases in oil prices are passed on to consumers especially quickly in Germany and that, together with the overall sharp rise in prices, this may indicate a lower level of competition in the fuel market.

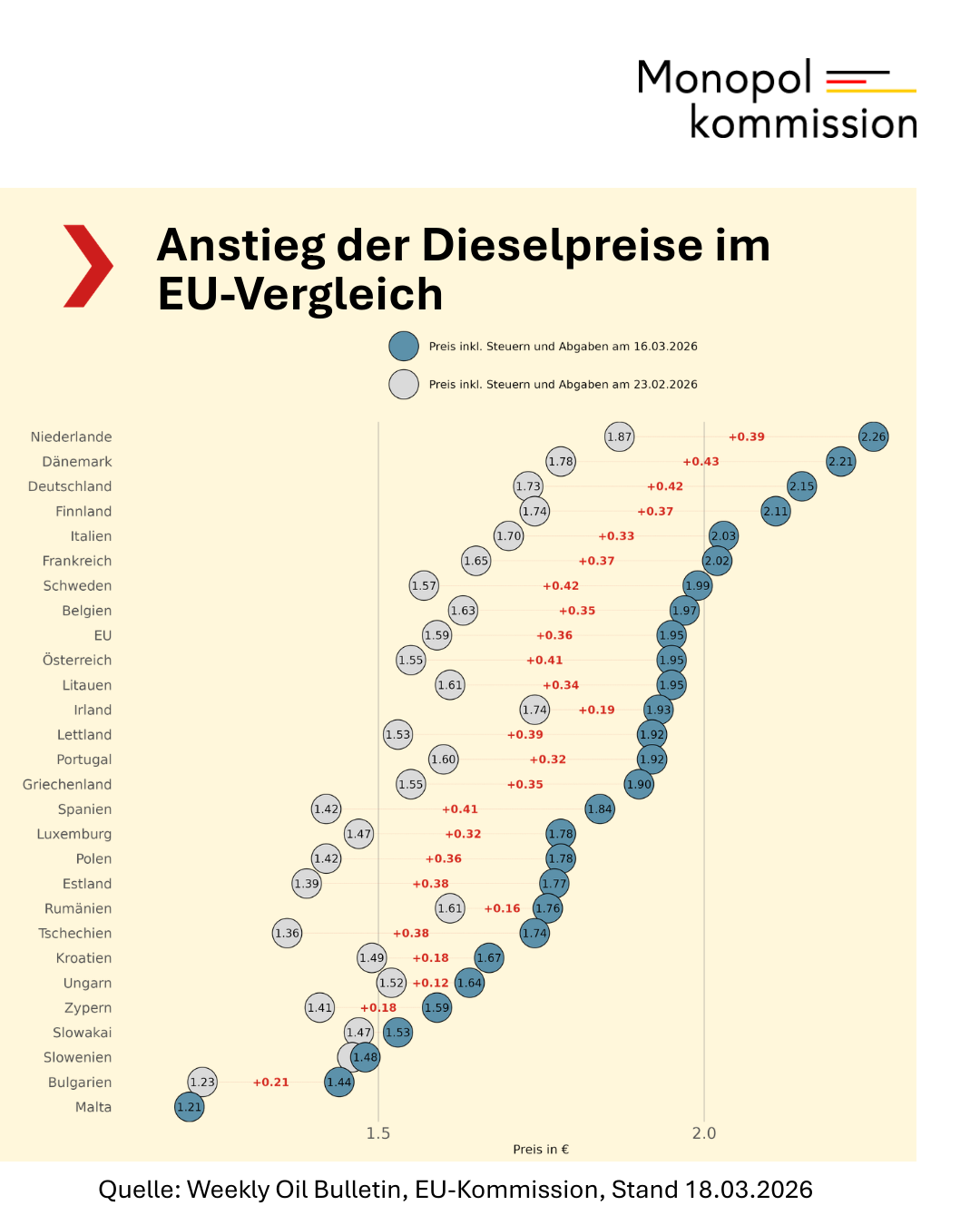

Image

(Source: Monopolies Commission)

The German government responded swiftly by fast-tracking a new law through Parliament, following consultations with renowned experts, including from the German Trade Union Confederation (DGB), the Monopolies Commission, Verbraucherzentrale Bundesverband, Justus Haucap (University of Düsseldorf), Jens-Uwe Franck (University of Mannheim), and Daniel Witzani-Haim (Arbeiterkammer Wien).

The new measures have received a mixed reception, with stronger support for the former Austrian model as a quick and not directly price administrative reaction – albeit with some nuanced changes proposed. These include adjusting the timing to 11:00 or the evening hours, which would benefit specifically free petrol stations, which would particularly benefit independent petrol stations, or splitting the country into two halves or regions to account for rapid assessments. Evidence from Austria, which has been operating such a model for quite some time, suggests that the effects are limited if the model is not combined with additional measures, such as price transparency mechanisms in consumer-facing apps that display only the cheapest petrol stations each day, thereby increasing competition among petrol stations.

Experts have divergent views on the two core-competition mechanisms. The following discussion is focussing on the two latter.

New exploitative abuse: Excessive mark-ups in the wholesale and refining fuel markets

The act introduces a new Section 29a German Competition Act to cover a sector-specific excessive pricing exploitative abuse in the form of excessive mark-ups in the wholesale and refining fuel markets. According to the new provision:

“A fuel supplier must not abuse a dominant position or relative market power in any market upstream of the supply of fuel to end consumers, whether held alone or jointly, by charging fuel prices that unreasonably exceed costs. In proceedings before the competition authority, the supplier bears the burden of proof regarding the allocation and level of costs and, where the level of costs significantly exceeds the market norm, also regarding the reasonableness of the costs.” (translation by the author)

The new provisions follows a similar but in details different provision in Section 29 German Competition Act that deals with energy markets (electricity, district heating or pipeline gas). It takes over the overall similar profit-limiting scheme. The new Section 29a appears to target the appropriate market level: refinery and wholesale fuel markets are highly concentrated oligopolies, whereas there is significant competition among petrol stations, particularly when taking independent operators into account. According to the Federal Cartel Office’s sector inquiry into refineries and wholesale fuel distribution, the fuel market is characterised by vertical integration, interdependencies, and limited contestability – conditions that generally hinder effective competition. Consequently, stricter oversight of potential abuses appears reasonable.

Dominance or dependence?

It is worth stressing, first, that the new provision Section 29a, contrary to Section 29 for energy markets, also applies in cases of relative market power. This significantly lowers the threshold for intervention, as it enables authorities to address structurally weak competitive conditions in oligopolistic settings without having to establish traditional dominance. In energy markets targeted by Section 29, situations of single-firm dominance are more common. By contrast, wholesale and refining fuel markets are characterised by oligopolistic structures with strong interdependencies, particularly affecting independent petrol stations.

Consequently, covering relative market power is particularly relevant in highly concentrated markets, where individual dominance may be absent and collective dominance difficult to establish, yet relative market power more accurately reflects market conditions and persistent dependency relationships. Such an approach seems to be crucial in oligopolistic fuel retail and wholesale markets characterised by the mentioned structural asymmetries, vertical integration, and limited contestability. In these markets, competitive pressure is weakened not through explicit market power, but through persistent entry barriers, upstream bottlenecks, and the lack of viable alternatives for independent trading partners. Relative market power, thus, captures forms of economic dependence that traditional dominance tests may overlook, especially where market outcomes are shaped by pricing mechanisms at earlier stages of the value chain, such as refining or wholesale.

At the same time, extending intervention to these scenarios raises difficult questions about how to distinguish between structural market outcomes and abusive conduct, particularly where price increases may also reflect crisis-driven volatility, risk premia, or supply constraints rather than exploitative behaviour.

Solving an underenforcement problem or price regulation?

A second key element is the reversal of the burden of proof in favour of the competition authorities with regard to cost levels and their reasonableness. This has attracted criticism concerning legal certainty and the risk of over-enforcement, particularly where cost-based abuse standards are combined with such a reversal, potentially turning relative market power into a quasi-presumption of abuse. What happens if companies are unable to sufficiently substantiate their costs? Are prices then effectively presumed abusive unless firms can demonstrate an adequate cost basis? Critics from the fuel industry also question how this approach aligns with the rule of law and, especially in the context of fines, with principles such as in dubio pro reo.

More fundamentally, this approach risks blurring the line between competition law and de facto price regulation. If authorities are required to assess the ‘reasonableness’ of prices based on incomplete or contested cost information, enforcement may shift from targeting exploitative conduct to supervising price formation itself. This raises concerns not only about legal certainty and administrability, but also about potential chilling effects on legitimate pricing behaviour in volatile markets, where cost structures are complex and rapidly changing.

At the same time, the reform addresses a genuine enforcement problem: regulators typically lack timely access to the same information on costs, risk premia, regional pricing, and internal pricing mechanisms as companies. From an enforcement perspective, a shift in the burden of proof is therefore understandable. Where high market concentration coincides with information asymmetry, expanding the authority’s scope for intervention may appear justified. It can strengthen the effectiveness of abuse control in markets where traditional tools have proven difficult to apply, particularly by enabling authorities to address situations of structural market power that fall short of dominance but nonetheless allow firms to sustain prices above competitive levels. In such highly concentrated markets with limited competitive pressure, a reversal of the burden of proof also, from a consumer protection perspective, require firms to justify significant price increases. The obligation to substantiate cost structures may also enhance transparency and accountability in price formation, potentially deterring opportunistic pricing behaviour in times of crisis. More broadly, the provision reflects an attempt to adapt competition law to markets characterised by persistent concentration, vertical integration, and limited contestability, where conventional dominance-based approaches risk under-enforcement.

The new ‘new competition tool’

Germany’s ‘new competition tool’ in Section 32f German Competition Act was first applied in the context of the fuel wholesale market. Now, fuel markets are the reason for renewing once again the new competition tool as a whole, i.e. not just in the context of fuel markets. The lengthy and hard-to-understand Section 32f (3) sentences 1 – 6 German Competition Act will be reduced to the following sentence:

“Where there is a significant and continuing malfunctioning of competition in at least one market covering the whole of Germany, several individual markets or across markets, the Federal Cartel Office may, insofar as the application of the other powers under Part 1 appears unlikely to be sufficient based on the information available to the Federal Cartel Office at the time of the decision, impose upon undertakings any behavioural or structural remedies necessary to eliminate or reduce the distortion of competition.“ (translation by the author)

Less procedure, more power?

As regards the reduction from the current three-stage procedure – (1) sector inquiry, (2) a finding of a significant and continuing malfunctioning of competition, and (3) the imposition of remedial measures – to two stages – (1) sector inquiry and (2) a finding of a significant and continuing malfunctioning of competition as well as the imposition of remedial measures – the reform may lead to greater procedural efficiency and more timely proceedings. While it removes the possibility of seeking judicial review against the finding decision alone, legal remedies with suspensive effect remain available at both stages.

Although the changes apply beyond fuel markets, this streamlining may be particularly valuable in markets where competition problems are structural and persistent, yet evolve more rapidly, especially in times of crisis, than traditional procedures allow. By reducing procedural fragmentation, the authority is better positioned to intervene before market distortions become entrenched. This may also enhance the effectiveness of sector inquiries as a policy tool, enabling them to lead more directly to remedies rather than prolonged intermediate steps.

At the same time, consolidating the stages increases the intensity of the initial decision and places greater weight on the evidentiary and analytical robustness of the authority’s findings, especially regarding the high standards of economic analysis, as both the diagnosis of a malfunctioning market and the choice of remedies are bundled into a single act. This reinforces the importance of procedural safeguards and judicial scrutiny at that stage, even if overall proceedings become faster.

From conduct to structure?

The removal of the requirement that addressees of remedial measures must have ‘contributed significantly to the malfunctioning of competition’, will also speed up and simplify proceedings. While the criterion served a certain proportionality function given the possible wide-ranging remedial function, the removal is consistent with the structural logic of the instrument. Section 32f (3) German Competition Act was supposed to be of market-structural nature, which is hampered by such individual assessment that may delay proceedings. Structural competition problems in concentrated markets often cannot be attributed to specific conduct by individual firms.

In this sense, the reform clarifies and reinforces the structural character of the instrument: intervention is no longer primarily linked to individual culpability, but to the existence of a persistent malfunctioning of competition at the market level. This may enhance the effectiveness of the tool in oligopolistic or otherwise structurally highly concentrated or problematic markets, where competitive harm arises from market configuration rather than identifiable misconduct of individual firms. Nevertheless, this shift reflects a broader reorientation of competition law from conduct control towards market structure governance, with corresponding implications for the justification and limits of regulatory intervention.

Conclusions

The competition measures in the Fuel Policy Package are economically sound, addressing genuine enforcement and structural problems. Precisely because of their potential wide-ranging impact, however, they raise heightened demands in terms of clarity, proportionality, and legal protection.

***

Parts of this blog are based on my presentation ‘Risks to Competition in Highly Concentrated Markets’ (Wettbewerbsgefahren in hochkonzentrierten Märkten) given on Monday, 23 March 2026 at the 18th Speyer Competition Law Forum (18. Speyerer Kartellrechtsforum) of the German University of Administrative Sciences Speyer (Deutsche Universität für Verwaltungswissenschaften Speyer). I thank Wolfgang Weiß for the invitation to the Forum, the participants for the timely discussion, and Maximilian Burger for his research assistance.

Comments (0)

Your email address will not be published.

Become a contributor!

Interested in contributing? Submit your proposal for a blog post now and become a part of our legal community!

Contact Editorial Guidelines

You may also like

March 31, 2026

{kind=link}

{kind=link}