In the last few months I have been deeply committed with the Klaus Vogel Lecture, which will be held in September 25, 2015, in the Vienna University of Economics and Business (see invitation here). I…

The establishment of a link between the financial interests of the Union and the general budget of the Union is the reason why the domestic penalties made applicable in matters of VAT fraud are…

China’s fiscal and tax reform should aim to narrow down income disparity and facilitate income redistribution to realize social equity. Justifiably, Chinese citizens’ perception to the rich has been…

In a recent post, Professor Werner Haslehner raised an interesting discussion on the new wording of Article 4.1 (a) of the Parent-Subsidiary Directive (“PSD”), which obliges the Member State of the…

In many respects a multilateral tax treaty represents an utopian view of international tax law: a wide consensus among nation states to submit themselves to a common set of rules that govern the…

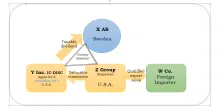

A Delaware company, which was a wholly owned subsidiary of a Swedish corporation (aktiebolag), acted as a non-independent agent on behalf of exporting companies in the United States. The profit of…

This post answers the emails received requesting further information on the US Competent Authority, including statistics, based upon my Kluwer Tax Blog post of 25 August IRS Issues New Competent…

Last month, Dennis Weber started a debate on recent BEPS-related changes to European tax directives with his post on the General Anti-Abuse Rule in the Parent-Subsidiary. I would like to follow up on…

This is another lone voice cry in the wilderness – I am getting used to that.

By 9 September 2015, anyone who has an opinion about further corporate tax transparency in Europe, are invited to file it…

Haydon Perryman’s exclamation this month, in the form of the above title, underlies that the FATCA GIIN update as of August 2015 is that there is little to update in terms of new GIINs. From July…