The raison d’être of corporate taxation relates to the aim of achieving an impartial treatment of different legal forms in order to safeguard a level playing field for conducting business. In the EU…

In order to close this cycle of dissertations about non-discrimination in International Tax Law, we will finish by talking about the specific case of the Andean Countries.

Decision 578 of the Andean…

An open door for emerging economies or the beginning of the end in international tax co-ordination

In an article published earlier this year,[1. Teijeiro, Opening the Pandora’s Box in the…

As from the first BEPS proposals with respect to intangibles, it has been considered that the Arm’s Length Standard (“ALS”) is “slowly but surely being relegated to the back seat” of the OECD…

In many European countries, the question of legal personality has relevance for determining the transparent character of a business entity for tax purposes and this assessment is even more complex…

In the last few months I have been deeply committed with the Klaus Vogel Lecture, which will be held in September 25, 2015, in the Vienna University of Economics and Business (see invitation here). I…

In many respects a multilateral tax treaty represents an utopian view of international tax law: a wide consensus among nation states to submit themselves to a common set of rules that govern the…

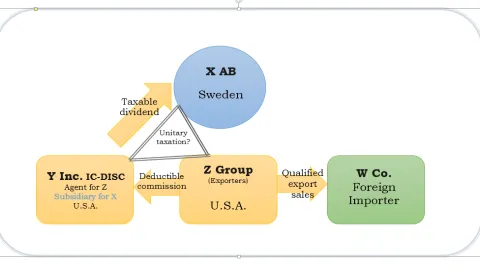

A Delaware company, which was a wholly owned subsidiary of a Swedish corporation (aktiebolag), acted as a non-independent agent on behalf of exporting companies in the United States. The profit of…

The case brings about the opportunity to fill a gap in the Norwegian tax law. In order to determine the fiscal residence of a corporation, the current formula stipulated by art. 2(2) Tax Act uses the…