In many respects a multilateral tax treaty represents an utopian view of international tax law: a wide consensus among nation states to submit themselves to a common set of rules that govern the…

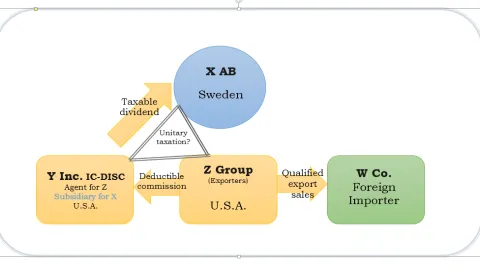

A Delaware company, which was a wholly owned subsidiary of a Swedish corporation (aktiebolag), acted as a non-independent agent on behalf of exporting companies in the United States. The profit of…

On august 7, 2015, OECD released its Update on Voluntary Disclosure Programmes: A pathway to tax compliance, a renewed edition of the survey published in 2010, aimed at providing guidance to…

The case brings about the opportunity to fill a gap in the Norwegian tax law. In order to determine the fiscal residence of a corporation, the current formula stipulated by art. 2(2) Tax Act uses the…

In line with BEPS Action 12, the Brazilian President enacted, on July 21, 2015, the Provisional Measure ("MP") no. 685, creating the obligation for taxpayers to disclose aggressive tax plannings…

Part 1 of the Report to G20 Development Working group (DWG) on the impact of BEPS in Low Income countries (LICs), dated July 2014, listed in its Section 6: Other High priority BEPS Issues for…

Co-authored with Hans van den Hurk, Maastricht University, QuanteraGlobal Tax Policy. Note that the authors write in their personal capacity.

Policymakers are changing the international tax system to…

Co-authored by Luís Eduardo Schoueri and Mateus Calicchio Barbosa

Spotlight was shed on transparency by the OECD’s BEPS Plan, where a set of Actions was put forward under the flag of “ensuring…

Article 7(1) of the OECD model treaty is perhaps the most important rule regulating the international taxation of business. It sets out the fundamental basis on which businesses are taxed, that is,…