The transition from bilateralism to multilateralism in regard of international law-making seems to be a relentless work in progress. Nobody contests that multilateralism would be – legally speaking –…

Harmonisation of the efforts to discourage tax avoidance in the EU

Recently, besides the objective of maintaining a balanced allocation1 (a reflection of the principle of territoriality), the…

The raison d’être of corporate taxation relates to the aim of achieving an impartial treatment of different legal forms in order to safeguard a level playing field for conducting business. In the EU…

According to EU law the prevailing divergences between the national tax systems shall not be corrected by unilateral measures that grant fiscal advantages to firms, which are affected by the…

The scope of the present article will be narrow. The aim is to point out a misinterpretation of the Cadbury ruling, which might have caused a flawed theory of the compatibility of certain CFC regimes…

In many European countries, the question of legal personality has relevance for determining the transparent character of a business entity for tax purposes and this assessment is even more complex…

The establishment of a link between the financial interests of the Union and the general budget of the Union is the reason why the domestic penalties made applicable in matters of VAT fraud are…

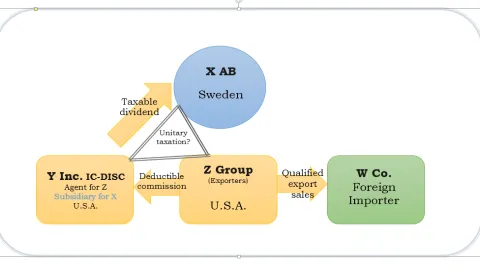

A Delaware company, which was a wholly owned subsidiary of a Swedish corporation (aktiebolag), acted as a non-independent agent on behalf of exporting companies in the United States. The profit of…

The case brings about the opportunity to fill a gap in the Norwegian tax law. In order to determine the fiscal residence of a corporation, the current formula stipulated by art. 2(2) Tax Act uses the…